Learn more about the comprehensive history of technology and how it has directly shaped the realm of investing. ...

Investment Corner with Jason & Sean: U.S. Small Cap Equities

Looking at the college graduating class of 2019, 69% of graduates had student debt with an average balance of roughly $30K. In addition, according to a study by New America (a nonprofit, nonpartisan think tank), the average interest rate on this outstanding student debt is roughly 5.8%, implying an average annual interest on student debt of roughly $1,700 per year before graduates even begin to pay down principal. With current outstanding student debt of roughly $1.7 trillion, up from $480 billion in 2006 with a nearly 9.5% annual increase, it is clear that student debt planning is a key financial planning topic.

Many students rely on the Federal Government for school loans, for which they may be eligible for any of the following: subsidized, unsubsidized, and PLUS loans. If a student is not eligible for Federal Government school loans, or those loans do not cover their full tuition balance, students may apply for private loans. The main differences between subsidized and unsubsidized loans are that students must demonstrate a financial need to qualify for a subsidized loan.

Direct Plus loans are only available to graduate/professional students and parents of dependent undergraduate students.

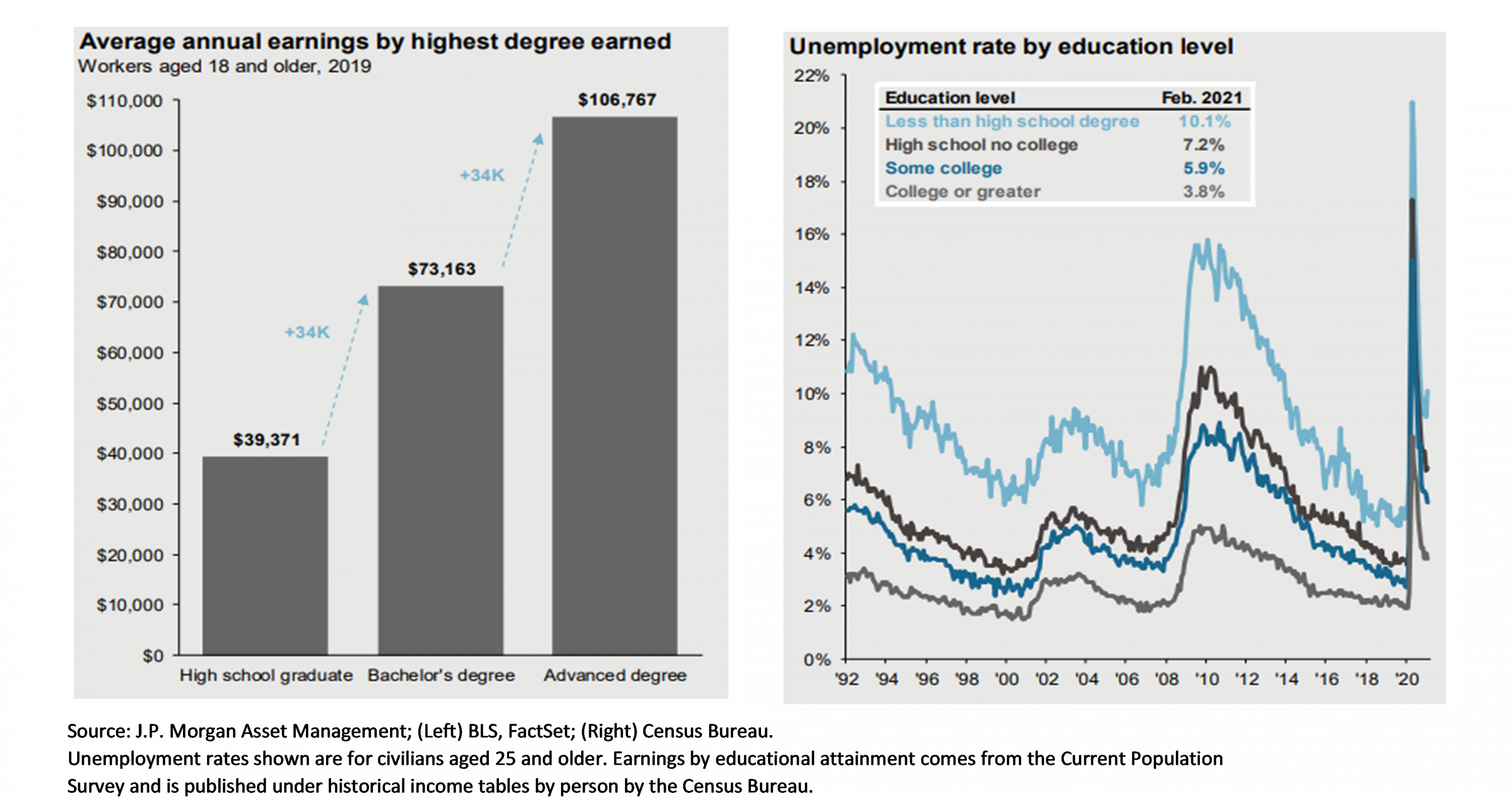

We will not be going in-depth on the recent “Is college worth it?” debate, but the data below makes a compelling case for the very positive impact of a college education on an individual’s long-term earnings potential in the workforce. As illustrated in the charts below, the average earnings and unemployment data for college-educated individuals paints a favorable picture relative to high school-only graduates. There is a caveat to the debate about whether to attend college or not.

The trick to navigating the college finance question is a clear understanding and plan for education prior to enrollment. Key college planning considerations include:

As student debt balances continue to balloon, having a plan in place coupled with a clear long-term vision is crucial in effectively managing student debt obligations. If you have questions about managing student debt that you’ve already incurred or are preparing for a child or grandchild to go to college, please reach out to one of our Schneider Downs Wealth Management Advisors.

Learn more about the comprehensive history of technology and how it has directly shaped the realm of investing. ...

Learn more about the top five new artificial intelligence features of wave one of the 2024 release of Dynamics 365 Business Central. ...

We’d love to hear from you. Drop us a note, and we’ll respond to you as quickly as possible.

Ask us

[email protected]

p:412.261.3644

f:412.261.4876

[email protected]

p:614.621.4060

f:614.621.4062

[email protected]

p:571.380.9003