Learn more about the comprehensive history of technology and how it has directly shaped the realm of investing. ...

Investment Corner with Jason & Sean: U.S. Small Cap Equities

Yesterday, after much speculation and fanfare, the House Committee on Ways and Means released a tax reform bill – the Tax Cuts and Jobs Act – that contains many of the same concepts that have been advocated for in the past. The bill exceeds 480 pages; this article only touches on certain highlights.

There have been two major aspects of tax reform that President Trump has not waivered on from the beginning, the first being that the impact on the middle class should be viewed as an overall tax cut. The GOP believes the new bill will save the average middle-class family money, though we are still analyzing the overall impact as to winners and losers. The debate of the issue will be now in full effect with the reveal of the complete tax bill. Stay tuned for news on how the bill is scored and how it stands to impact the economy.

The other aspect is a reduction in the corporate tax rate. The House bill does reduce the rate to the 20% President Trump requested.

Other major concepts in the bill that will affect many Americans include:

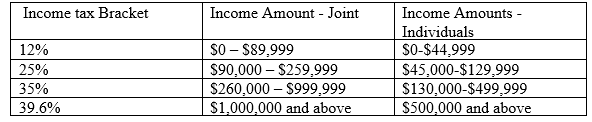

1.) A reduction in the number of individual income tax brackets. The bill enumerates:

2.) Enhancement of the standard deduction.

3.) Repeal of personal exemptions,

4.) A maximum tax rate of 25% on portions of qualifying flow-through business income.

5.) The State and Local Income Tax deduction has been eliminated.

6.) The State and Local Real Estate Tax deduction is limited to $10,000.

7.) The bill preserves the interest deduction for existing mortgages, but caps the deduction at the first $500,000 on mortgage debt for newly purchased homes.

8.) The child tax credit is increased to $1,600 per child under the age of 17 and includes an additional $300 credit for each parent as part of a consolidated family tax credit.

9.) A noted area of “no change” from the current tax law is in the area of retirement savings. The bill does not change pre-tax levels for retirement accounts.

10.) The alternative minimum tax is repealed for all future periods.

11.) Repeal of the estate tax.

Another concept that has been consistent throughout tax reform discussions over the past 18 months are provisions that encourage capital investment in the U.S. by business. The proposed bill accomplishes that goal by allowing immediate expensing of the cost of qualified property placed in service after September 27, 2017, and before January 1, 2023. There is, however, an offset to that provision that places limitations on the deductibility of interest for most companies in excess of 30% of taxable income. Below are some of the major business provisions:

In summary, there are many new provisions in the bill that impact individuals, corporations, partnerships and tax-exempt organizations, but there likely will be a number of changes as negotiations occur between Democrats and Republicans and between the House and Senate. Further, more detailed analysis from think tanks, consultants, individuals, businesses, lobbyists and others, all advocating for or against certain positions, will also likely result in further negotiation and change.

As these proposals evolve and a final bill is presented to the president for signature, we will continue to analyze the projected – and, ultimately final – legislation to keep you updated on the impact to you and your business.

Please return to the Our Thoughts On…Tax Reform blog for updates as they become available.

Learn more about the comprehensive history of technology and how it has directly shaped the realm of investing. ...

Learn more about the top five new artificial intelligence features of wave one of the 2024 release of Dynamics 365 Business Central. ...

We’d love to hear from you. Drop us a note, and we’ll respond to you as quickly as possible.

Ask us

[email protected]

p:412.261.3644

f:412.261.4876

[email protected]

p:614.621.4060

f:614.621.4062

[email protected]

p:571.380.9003