Learn more about the comprehensive history of technology and how it has directly shaped the realm of investing. ...

Investment Corner with Jason & Sean: U.S. Small Cap Equities

The Tax Cuts and Jobs Act represents the largest overhaul in federal tax law since 1986. The changes are sweeping and affect almost every form of income tax on the books. Under the new law, most individuals and corporations will see a decrease their tax rates, which likely could mean a decrease in their overall tax liability.

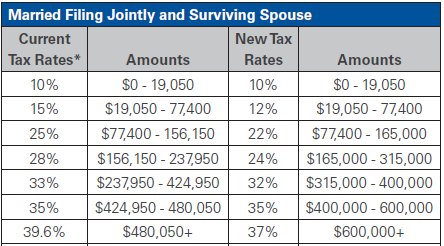

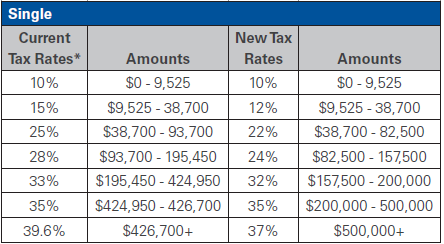

Changes to Individual Income Tax Rates

The Act includes a number of major changes to the rules on individual income taxes, including a new pass-through business income deduction, a repeal of the personal exemption, and an increase to the standard deduction. However, one of the most important of these changes is the revised tax rates for the seven marginal tax brackets. We’ve provided a comparison of the rates expected for 2018 under the old law compared with the Act’s new tax rates for married filing jointly and single filing status:

Under the new law, taxpayers in six of the seven brackets are now subject to lower tax rates. Most notably, taxpayers in the highest bracket now benefit from a 2.6% decrease in their marginal income tax liability.

Changes to Corporate Tax Rates

Under the Act, the new corporate tax rate is a flat 21%.

Under prior law, corporations and their shareholders paying income tax in the United States were potentially subject to a combined income tax rate of 50.47%. This percentage is comprised of two taxes: 1) a 35% entity-level corporate tax rate, and 2) a 23.8% shareholder-level tax rate on the remaining 65% of corporate income distributed as a dividend (35% + [65% x 23.8%] = 50.47%).

With this new rate of 21 %, these taxpayers now enjoy a lower combined tax rate of 39.8% (21% corporate tax plus 23.8% tax on remaining 79% of corporate income distributed as a dividend).

Should you review your choice of entity – C versus S corporation?

It is important to note that despite the change in the entity-level corporate tax rate, the difference in tax rates between C-corporations (subject to the entity-level tax and a tax on dividends distributed) and S-corporations (a pass-through entity) remains about 10%. This maintained rate difference is due to the Act’s changes to the individual income tax rules including the inclusion of a new 20% qualified business income deduction.

Under prior law, S-corporations were subject to a top combined tax rate of 40.8%. This rate was comprised of a top marginal individual tax rate of 39.6% plus a 1.2% itemized deduction limitation. With the passage of the Act, the top individual marginal tax rate is now lowered from 39.6% to 37%. On top of that benefit, the Act also grants S-corporation shareholders a new 20% qualified business income deduction towards their individual income liability. With these changes, S-corporations now enjoy a significantly lower combined tax rate of 29.6% (the product of the 37% top marginal individual tax rate reduced by the 20% pass-through income deduction). The new 20% deduction is subject to several limitations and restrictions and may not apply to all situations.

Applying pre-Act law, the C-corporation combined rate of 50.47% was approximately 10% higher than the S-corporation rate of 40.8%. With the Act now in effect, the C-corporation combined rate of 39.8% is still approximately 10% higher than the S-corporation rate of 29.6%. Every situation can be different, so the best course of action would be to discuss any changes with your tax advisor and run the numbers.

If you have questions about this article, please contact us. For similar articles, please visit the Out Thoughts On...Transportation and Logistics blog.

Learn more about the comprehensive history of technology and how it has directly shaped the realm of investing. ...

Learn more about the top five new artificial intelligence features of wave one of the 2024 release of Dynamics 365 Business Central. ...

We’d love to hear from you. Drop us a note, and we’ll respond to you as quickly as possible.

Ask us

[email protected]

p:412.261.3644

f:412.261.4876

[email protected]

p:614.621.4060

f:614.621.4062

[email protected]

p:571.380.9003