Learn more the $16M scandal surrounding MLB pitcher Shohei Ohtani's former interpreter Ippei Mizuhara. ...

Lost in Translation: Ippei Mizuhara Accused of Wire Fraud in Excess of $16M

Several stakeholder groups, including the AICPA, FASB NFP Advisory Committee and others, have raised concerns over the difficulty encountered by many not-for-profit entities in applying the current guidance around accounting for grants and contributions. These groups have cited significant diversity in practice over the interpretation of the rules in the following two areas:

On August 3, 2017, the FASB released a proposed accounting standard update to help clarify the accounting rules around these issues and eliminate the diversity within the sector. The proposal provides the following suggested improvements.

Exchange Transaction or a Contribution:

The proposed amendments would clarify how an entity determines whether a resource provider is participating in an exchange transaction by evaluating whether the resource provider is receiving commensurate value in return for the resources transferred on the basis of the following:

Conditional verses Unconditional Contribution:

The amendments in this proposed accounting standard update would require that an entity determine whether a contribution is conditional on the basis of whether an agreement includes a barrier that must be overcome and either a right of return of assets transferred or a right of release of a promisor’s obligation to transfer assets. The presence of both a barrier and a right of return or a right of release indicates that a recipient is not entitled to the transferred assets (or a future transfer of assets) until it has overcome the barriers in the agreement.

Indicators would be used to guide the assessment of whether an agreement contains a barrier. Depending on the facts and circumstances, some indicators might be more significant than others, and no single indicator would be determinative. The indicators would include:

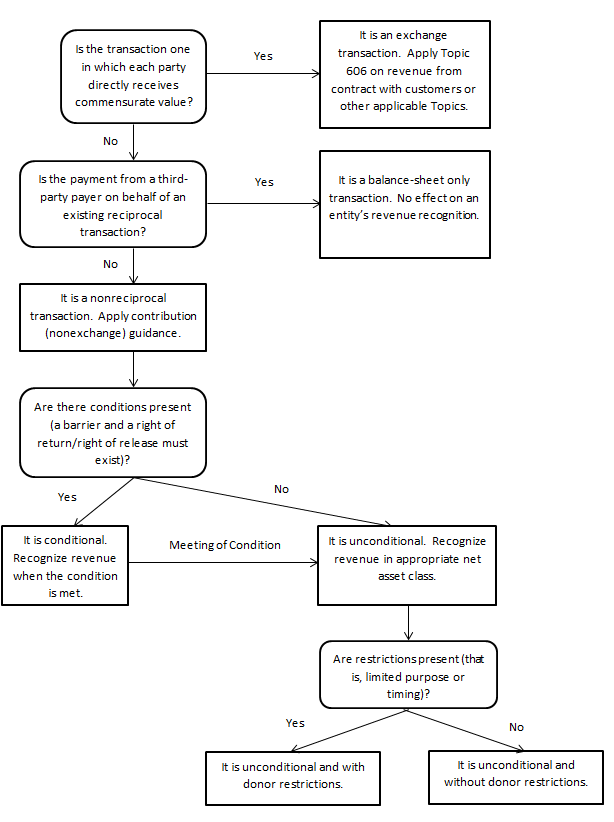

The FASB’s proposal includes the following diagram to illustrate the process for determining whether a transfer of assets to a recipient is a contribution or an exchange transaction and how to distinguish between a conditional contribution and an unconditional contribution. The diagram also illustrates whether there is an associated donor restriction with an unconditional contribution.

Proposed Effective Date and Comment Period:

The effective date of the amendments in this proposed update would be the same as the effective date for the new revenue recognition rules under FASB ASU 2014-09 and ASU 2015-14. A public business entity and an NFP that has issued, or is a conduit bond obligor for, securities that are traded, listed, or quoted on an exchange or an over-the-counter market would apply the amendments in this proposed accounting standard update to annual periods beginning after December 15, 2017. All other entities would apply the amendments in this proposed accounting standard update to annual periods beginning after December 15, 2018.

The FASB invites individuals and organizations to comment on all matters in this proposed update by November 1, 2017. A final pronouncement is expected to be issued in 2018.

If you have questions about the proposed improvements, please contact us.

Learn more the $16M scandal surrounding MLB pitcher Shohei Ohtani's former interpreter Ippei Mizuhara. ...

Learn more the $16M scandal surrounding MLB pitcher Shohei Ohtani's former interpreter Ippei Mizuhara. ...

We’d love to hear from you. Drop us a note, and we’ll respond to you as quickly as possible.

Ask us

[email protected]

p:412.261.3644

f:412.261.4876

[email protected]

p:614.621.4060

f:614.621.4062

[email protected]

p:571.380.9003